Expected Moves & Vol Crush

Last year, I wrote a series of blogs on vol crush, i.e., the tendency for the implied volatility of certain stocks to fall after earnings announcements or other scheduled events. You can find them here and here. Vol crush is especially pronounced in stocks very sensitive to earnings reports (tech), drug trial or regulatory announcements (bio tech), or legal rulings to be announced on a specific date.

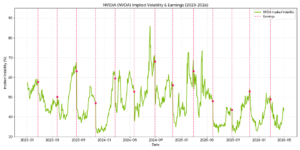

Nvidia presents a great example of the phenomenon:

As you can see, vol crush is significant and consistent and occurs after almost every earnings announcement.

Reviewing the chart, it’s tempting to believe that a short volatility strategy, e.g. short straddles or strangles, can profit from vol crush. Unfortunately, it’s not that simple. The question is whether the potential move in implied volatilty, coupled with time decay, will be enough to counteract the potential move in price. Or, in options speak, can you keep the position’s gamma under control?

Unfortunately, in almost all instances, the answer is “no.” After performing a simple backtest on NVDA of a short straddle strategy using short‑dated (3‑day DTE) options executed at the close before the earnings announcement, the results show that, despite the steep and consistent post‑earnings volatility crush, losses from large price moves typically overwhelmed the gains from declining implied volatility. Of the 25 earnings events since 2020, short naked straddles lost an average of 69%, with one trade in May 2023 losing a whopping 505.6%. I should note that the backtest assumed no delta-hedging and that the straddle was “naked” when executed, something that institutional volatility traders would rarely do.

But here’s the good news. If the short straddle strategy failed, the opposite would be true: long short-dated NVDA straddles going into earnings announcements gained an average of 69% since 2020. Performing the same backtest on a stock that displays similar vol crush, Palantir (PLTR) yields similar results and confirms that the short straddle strategy is not a profitable strategy (and that’s an understatement). Flipping the strategy to the long side, however, returns an average of 95% (median 67%) since 2020.

Regardless, let’s say that you are considering a selling, or buying, naked straddles before an earnings announcement. How would you go about analyzing the trade?

The first step would be to determine the market’s estimate of the stock’s expected price range until expiration, or the implied move. There are a few ways to calculate this:

1) The quickest method is to use the at-the-money straddle for the expiration in question. Add up the put and call premium, and the expected move will be +/- that amount. If you want to be conservative, you can adjust the range downward if you wish.

2) More technically, you can use the implied volatility of the specific expiration: Expected Move = Stock Price * Implied Volatility * SQRT (Days to Expiration/252).

3) Some traders can better relate to daily expected moves. Take the implied volatility and divide it by 16 (roughly, the square root of 252, which is the typical number of trading days in a year). The resulting percentage is the daily implied move.

The next step is to estimate how large a decline in implied volatility would be required to offset the expected move in the underlying. An implied volatility to price move breakeven can then be determined. As we’ve seen in the NVDA chart above, even in cases of an earnings surprise, implied volatility usually decreases as the uncertainty surrounding the stock is eliminated. The downward moves have been consistent, with 1-day moves post announcement averaging 10 to 16 vol points. But since prices also move considerably, the trick is to figure out whether they are large enough to counter the price move. Unfortunately for those that normally sell straddles, the answer is almost always “no.”

Prediction Markets

Prediction markets continue to get a lot of press. An article in the WSJ, Why Almost Everyone Loses—Except a Few Sharks—on Prediction Markets, (May 4) concludes that just 0.1% of Polymarket bettors make 67% of the profits and that are mostly high volume algorithmic players. It goes on to profile some participants that experienced tragic (but very predicable) losses from so-called “mention markets” (bets on what a celebrity or politician will say). It makes you wonder what benefit these markets serve. For a very good analysis of the question, read Are Prediction Markets Good for Anything? (Asterisk, Dan Schwartz, April 2026). His conclusion: maybe, but AI might make them obsolete.