War, Again and Again

I had intended to write this week’s blog about 0DTE options and their effect on the market. Sadly, the war in the Middle East is now center stage. As I wrote at the beginning of the war in Ukraine, I’m not a political analyst and can’t add much to political or strategic commentary available elsewhere. I will add one thing, however. 700 Israelis, mostly civilians, were killed during the first day. Israel has a population of 9 million, so that’s about .009% of the population. Given the current population of the US at approximately 340 million, that would be equivalent to over 26,000 people. A shocking statistic, to say the least.

It seems trivial and callous to talk about how the war has changed investment prospects, but this is a blog about finance and options. With that apology, let’s talk about the most obvious candidate to be affected by the war, crude oil.

Crude oil is now part of the so called “fear trade,” which includes the VIX, the US dollar, and gold. Past wars in the Mideast have included supply disruptions, so the first and logical reaction is to expect a spike in crude oil prices, at least in the short term. The market still remembers the oil embargos and supply curtailments of the 1970s.

However, this time there is an alternative narrative that could confound the crude oil bulls and the market. Iran and Saudi Arabia are rivals, and the latter has been negotiating the normalization of relations with Israel for some time. The war is obviously a setback to this, and to the extent that Iran was involved in arranging it, the Saudis will not be happy that once again their rival in the region has gained the upper hand. In response, they could use the only weapon they have available, crude oil prices, and turn the spigots wide open, starting an oil price war that would harm Iran where it hurts the most.

Of course, this scenario is pure speculation at this point and, at this point, a low probability outcome. The war is in its early days and the situation is in flux. Also possible is that the Biden Administration, in an effort to punish Iran for its involvement, starts enforcing the sanctions on oil that they have been previously been ignoring in an effort to arrive at a new nuclear agreement with Iran. Needless to say, any US/Iran negotiations are now dead. At the same time, any US reaction to the war that would increase oil and gasoline prices, and inflation, is certainly not what the Administration desires.

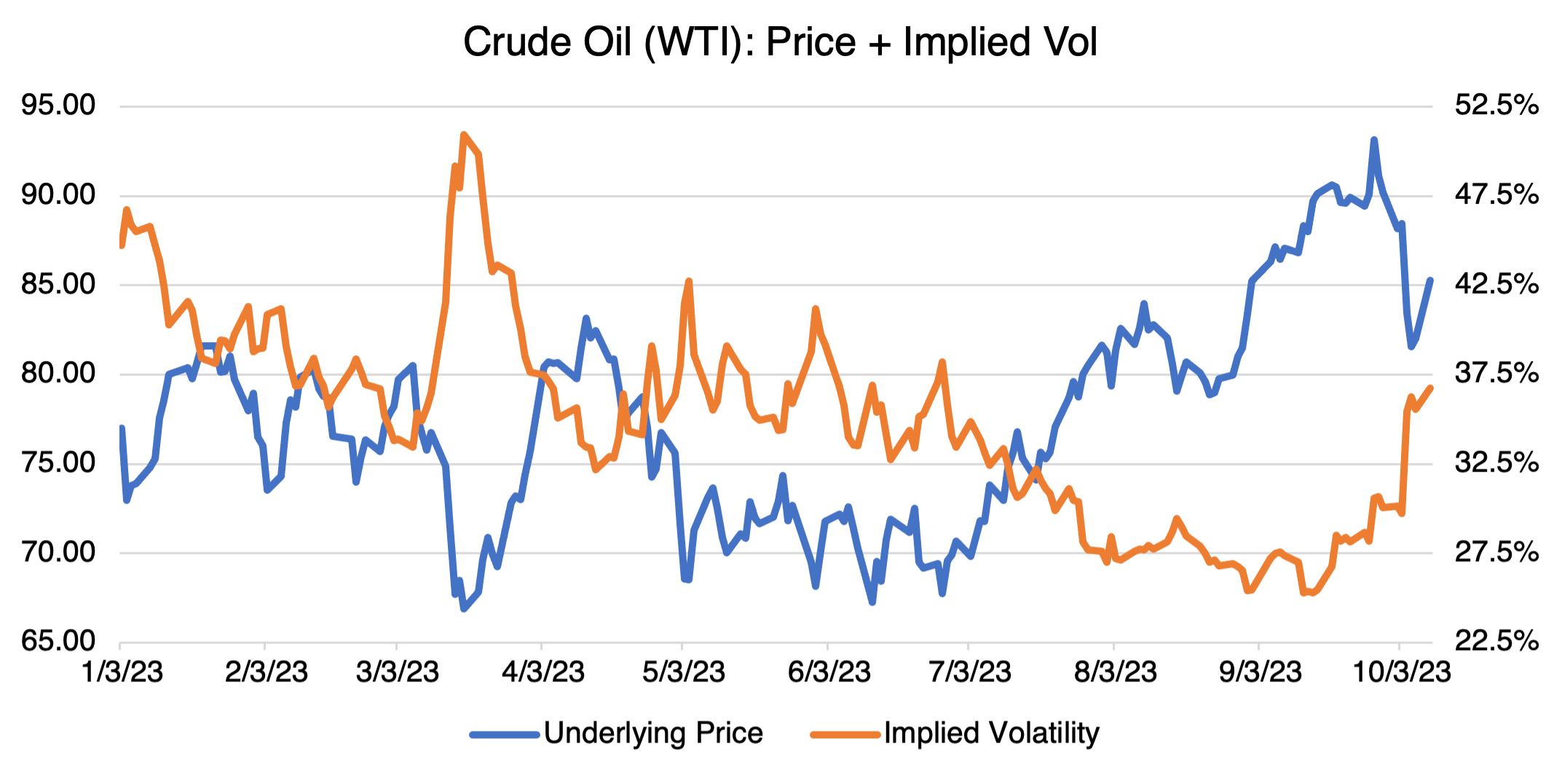

Trust me, no one knows what could develop. The only thing that is certain at this point is that uncertainty will rule. Since uncertainty is a major component of implied volatility, options will be affected. Similar to many stocks that we have reviewed, implied volatility and price are inversely related in crude oil (both Brent and WTI):

Source: OptionMetrics

The inverse relationship is very significant. Since 2005, IV at relatively high price levels is 4.5 times higher than at low levels:

| Price Range ($) | Average Implied Volatility (%, 30-day) |

|---|---|

| 0-25 | 141.8 |

| 25-50 | 47.0 |

| 50-75 | 33.7 |

| 75-100 | 31.7 |

What does this mean in practice? When prices are high, calls and puts are relatively inexpensive. Hence, the ongoing interest over the last few months in the $100 call. The opposite is also true: when prices are low, crude oil options become expensive. There are also ramifications after the trade is executed. If you believe crude oil prices are going to decline and buy puts, implied volatility will boost the value of your options as crude moves lower. Winning on price and implied volatility at the same time is one of the goals of options trading.

But, beware, the opposite situation can also occur. Holders of the $100 call, even if they are right and crude punches through that level, will in most circumstances have implied volatility working against them, or at least not helping. In that case, you will be in the frustrating situation of having called the market correctly but stuck with a suboptimal trade (as they say in risk management).

Of course, volatility is susceptible to significant short term shocks that can simply overwhelm how it behaves in normal markets. For example, Monday’s price action in crude oil, natural gas, and energy and defense stocks was so severe that it produced a significant upwards move in implied volatility, regardless of the normal inverse relationship. Similarly, expansion of the war to include Lebanon or even Iran could lead to an “all bets are off” situation that spikes implied volatility. That is, at least in the short term, or until the normal price/volatility relationship reestablishes itself. Usually, the initial upwards reaction in volatility is followed by a reversion to previous levels if new shocks or information are not forthcoming. As I discussed last week, the VIX usually follows this pattern, consistently disappointing knee jerk VIX buyers.

Next week, and barring any new and terrible news from the Mideast, I will return to 0DTE options and their potential effects on the markets.