VIX Futures: Watch the Shape!

If you’ve ever bought the VIX because things seem to be unraveling fast, you know it can be a frustrating experience. Just when it seems like the index is going to make a significant move to the upside, it backs off and slides back into the teens. Unrealistic expectations, mean reversion, and how the index is measured all contribute to this. So how can you tell whether a VIX rally is going to be short-lived or the real thing?

One way to help determine this is to look at the shape of the VIX futures curve. Since futures products have multiple contracts with different maturities, it’s possible to construct curves that display prices vs time to expiration. They may then be described by their overall shape and slope. When nearby expirations are trading at a premium to later maturities, the futures curve will be downward sloping, or backwardated (sometimes known as inverted). The reverse – nearby expirations trading at a discount to more deferred contracts – is known as contango. For commodities that can be stored, that is usually the case.

For cash-settled financial products, such as VIX futures, the shape of the curve is determined mostly by sentiment, the value of the VIX index itself, and the direction of the nearby contracts. During uncertain times, or in the case of extreme uncertainty or possible market declines, backwardation can occur because traders naturally concentrate on current market conditions and crowd into the nearby contracts, thereby bidding them up in relation to longer-term expirations.

VIX futures usually trade in contango. In general, the VIX curve only moves into a backwardated shape if the market is under extreme stress and the index itself is at relatively high levels. Since 02/24/2006, the VIX curve was backwardated only 18.8% of the time, mostly during the financial crisis (2008-2009) and during the depths of the pandemic (March, 2020). Backwardation is relatively rare, and something to take notice of when it does.

What may we infer from the current shape of the VIX futures curve?

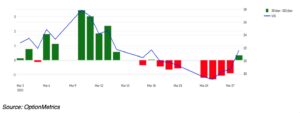

First, the curve (see chart below; backwardation = negative values, in red, contango = positive values, in green) is displaying behavior that usually indicates bearish, or extremely unsettled, conditions.

VIX futures were backwardated for the first half of March, reaching 3.45 on March 10th; the last time the market was backwardated greater than 3.00 was on 10/01/2020, during the pandemic. After returning to contango during the second half of the month, backwardation returned last Friday. That is not the sign of a healthy market.

Second, since backwardation is usually associated with high VIX levels, and the VIX generally moves inversely to the S&P 500, the curve may be indicating more negative equity swings to come.

GameStop: Meme on Meme!

Before writing about GameStop’s latest iteration, I must admit that I never really signed on to the whole meme stock thing. To me, it always seemed like a dressed up momentum trade, which when you get right down to it, amounts to buying things that are going up and selling things that are going down (it’s not as simplistic as it sounds; like the weather, some academic studies have concluded that the best indicator of stock performance over the next 3 to 12-month period is the previous 3 to 12-month period). With momentum trading, the trend is your friend, and the actual fundamentals of the company or asset don’t really matter that much. When momentum and meme stock strategies combine, the object is to get people to believe in the company, with almost religious fervor, and to maintain upward price momentum.

Which brings me to GameStop (GME) and how management is doubling down on its original meme/momentum strategy. Borrowing from Strategy’s (formerly MicroStrategy) business plan, GameStop announced last week that it would begin buying bitcoin as a treasury reserve asset. In order to fund the purchases, they will be selling $1.3 billion of convertible notes. Apparently, the company is trying to pivot from its core business of selling video games to buying (and holding) bitcoin. You have to admire GameStop’s consistency – the original meme ran out of gas, so now let’s try a new one!

GME shot up over 11% last Wednesday after the announcement of the new strategy. By Thursday, however, the stock came off 22% as traders came back to earth.

Since selling video games from retail locations is not exactly a growth business, GameStop needed something else to remain viable, and since it’s the memeyist of all meme stocks, what better route than latching on to the latest meme, buying bitcoin as a reserve asset using convertible debt. Basically, issue debt, use the proceeds to buy bitcoin, and then repeat until bitcoin is the company’s main (and sometimes only) asset. Like Strategy, the object is that the company’s market capitalization will exceed that of its bitcoin holdings. In other words, turn the company into a leveraged hedge fund with just one buy-and-hold asset in the portfolio. If you wouldn’t invest in a fund with that strategy, I don’t blame you.