The War & Some Surprises

The war in Iran is entering its second month and its effects on the markets have been well-covered by the financial press. However, there have been some reverberations that have slipped through the net, mostly because they are too subtle or specialized for a general audience.

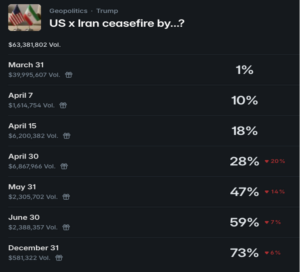

Last week, I focused on when the war will ramp down according to the prediction and futures markets. Since then, and since hostilities show no sign of abating, the odds of a ceasefire have decreased. Last week, the probability of ceasefire by March 31 was 20% and by the end of April, 50%. Below are the odds as of Monday morning:

Source: Polymarket

Evidently, the prediction market is a lot less sure of a near-term solution than it was last week. The probability of a ceasefire by June was 69% last week; on Monday, it was down to 60%.

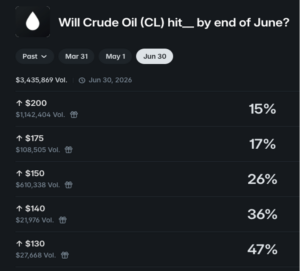

If you think that the war will still be going on in three months, and that the Straits will remain effectively closed, then you should also bet on super high oil prices. The resulting combination of shut-in production damage and lack of supply will probably drive the market to previously unthinkable highs. Of course, political factors will likely force a solution before that occurs. But, you never know – betting on what politicians are going to do is rarely a good idea. If you think that the war will go on longer than anticipated, then these could be for you:

Source: Polymarket

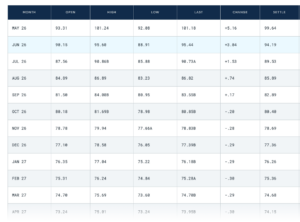

But…here’s something surprising given all the “forever war” news. Last Friday, deferred contracts in crude oil futures (WTI), starting with the October ‘26 contract, settled lower for the first time since the war began (see table below). The pattern repeated itself on Monday. Obviously, given the supply situation, the curve is still steeply backwardated. However, the decrease in back dated contracts in the face of sharply higher nearby months suggests that the futures market is increasingly certain that the dire supply situation will resolve itself roughly itself by Q3. That’s still roughly in line with what the prediction markets are saying.

Source: CME

Another subtle, and somewhat scary, effect of the war: correlation has skyrocketed. The CBOE COR3M index, which measures 3-month correlation of the SPX vs. its top-50 component stocks, has exploded since the war began and now stands at over 34, its highest level since the tariff scare of last April:

Source: CBOE

Why is this important? Because higher correlation means that stocks are moving in tandem, which is usually associated with periods of high stress and volatilty. Looking back, all periods of significant declines were accompanied by sharply higher correlation figures. Granted, you don’t really need COR3M to tell that we’re in a stressful market, but it’s one more metric that’s worth keeping an eye on just in case it reverses.

Someone Still Cares About Peloton!

Despite the war and various other genuine earth-shaking events, the world keeps on spinning. As evidence of that, last week Peloton (PTON) broke back into the news.

When I first started writing this blog about 5 years ago, Peloton went from being a Covid-era darling (we’ll never be able to leave the house!) to an overpriced clothes horse that costs $50 bucks a month. Like many other covid stocks suffering from over expansion and high fixed costs and a stock price a fraction of what they enjoyed in their heyday, the challenge is how to recover and “reinvent” themselves.

Almost four and half years and three CEOs later, Peloton is still trying to convince investors that they’ve figured it out. Improving margins, a move into commercial gyms, and some leadership changes are not doing the trick. For example, last Friday PTON gained 8.9% on the back of its announcement. On Monday, it gave back all its gains and then some, falling 9.7%. YTD, it’s down almost 35% and has been steadily declining since last October. On an options basis, PTON’s implied volatility is trading at roughly 150%, so its options are very expensive. It’s not a pretty picture.

Source: OptionMetrics

Will Peloton finally pull off its recovery? Other than continued problems with the business itself, they are facing challenging external factors. If the war continues longer than expected, and gasoline prices continue to spike, discretionary spending and consumer sentiment will suffer. Regardless of whether it’s true or not, Americans use gas prices as an indicator of their economic and social well-being. Low gas prices = everything is ok and inflation is under control; high and spiking gas prices = I’m running out of money, and the world is spinning out of control! In the latter scenario, Peloton enters the category of expenses that can be cut back. For similar reasons, PTON may be one of the first to be thrown over the side when investors go into risk-off mode.