The Market Isn’t “Wrong”

Last week, we saw a growing number of articles arguing that the oil futures market is somehow “disconnected,” “dislocated,” “unrealistic,” or just plain “wrong.” Participants are reportedly “shocked,” frustrated, and concerned about the market’s “lack of price discovery.” Social media is ablaze with conspiracy theories about manipulation and backroom deals designed to keep prices from spiking. In short, because the futures market isn’t behaving the way many commentators think it should, they assume something nefarious must be going on.

I’m not going to get into the worrying supply/demand situation that’s driving crude oil right now. It’s well-covered elsewhere. Suffice it to say there is no doubt that the closure of the Straits is having a catastrophic effect on supply that will not resolve itself anytime soon. Since the Strait accounts for roughly 20% of world oil supply, it’s easy to conclude oil should be trading significantly higher than it is today—and hard to find anyone who disagrees. Their argument is compelling. For each day that the Strait is closed the supply deficit gets worse, as do frenzied predictions of $200 oil and equity market destruction. Even if the Strait reopens soon, supply will still be disrupted for months to come.

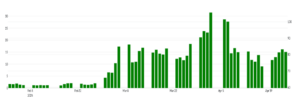

And yet, the war has been going on for more than two months, and the most extreme predictions still haven’t materialized. If the super-spike thesis were going to play out through lost barrels, we likely would have seen it by now in outright prices. Those predicting a super-spike might have been half right. Oil prices are meaningfully higher: WTI and Brent are up 39.9% and 38.3%, respectively, versus pre-war levels (02/27/2026). And physical shortages in the short-term market have caused backwardation to surge to record levels (see chart below):

Crude Oil (WTI, Continuous Futures): 6-month to 1-month Backwardation

Source: OptionMetrics

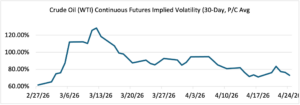

Finally, crude oil (WTI) implied volatility (see chart below) surged to a peak of 128.5% only 10 trading days after the start of the war, a full 55.5 vol points higher. Evidently, the market reacted, just not as much as the uberbulls expected. [As an aside, note that since their peak in early-March, both backwardation and implied volatility have moderated considerably, although both remain at elevated levels.]

Source: OptionMetrics

It’s entirely possible the futures market has already priced in much of the war’s impact. And as for the spillover to the global economy, oil’s share of total energy supply has fallen from roughly 50% in the 1970s to about 30% today. Crude oil is just not as impactful as it used to be. Of course, if the war expands to include energy infrastructure, the super-spikers might finally be proven right. However, even in that case, massive global demand destruction could mitigate the effect.

Just as many are surprised crude isn’t much higher because of the war, they may be even more surprised by what happens after it ends. Here’s one plausible bearish scenario:

- In energy markets, shortages often sow the seeds of the next glut.

- Once supply constraints ease, aggressive restocking can keep prices supported—until inventories and reserves are rebuilt.

- At the same time, higher prices pull forward supply: new extraction technology gets deployed, physical storage expands, and the war accelerates the trend away from crude. The combination can create meaningful downward pressure once the restocking impulse fades.

My advice to anyone who claims the market is “wrong” or malfunctioning is simple: ask whether you’re ignoring conflicting evidence—or just being stubborn. It’s tempting to believe you’ve outsmarted the market, but that’s rarely the case. Respect the market. It’s the most valuable clearinghouse of information we have, even if it doesn’t always behave the way we expect.