The Market is Weird?

“We should be adding here, not cutting!”

“The market is acting weird. I’ve never seen this before!”

“The market will turn around soon. I just need more time”

“You just don’t understand this position”

“The limits don’t make any sense”

“I’m going to hedge it with…”

“I’m having a great year. I can afford some losses!”

What do all these quotes have in common? They are all things I’ve heard from traders that are confronted with losing positions. As a former risk manager, it was my job to monitor performance and enforce limits, to be the heavy that forces traders to cut positions involuntarily. Believe me, it was never a pleasant experience, but it was always interesting to hear their justifications. Usually, they involved some combination of arrogance (“you just don’t understand what I’m trying to do!”), the sunk cost fallacy (“I’ve come this far, I might as well see it out”), over complication (“I’m going to hedge it”), or wishful thinking (“the market feels overextended, it’s going to go my way”). Individual traders aren’t immune to this type of fallacious thinking; I’ve seen large institutions faced with staggering losses do exactly the same (“let’s ringfence it so we can track it”).

Almost always, the root cause of the losses in question was that something was going on that the trader, investor, or institution just couldn’t figure out, despite their best efforts and opinion to the contrary. Since that was the case, any attempt to fix, mitigate, or wait out the situation wasn’t going to work. Almost always, cutting and starting over was the only solution.

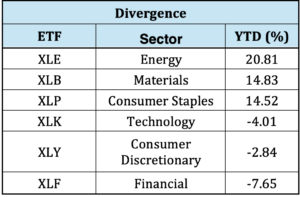

I thought of all this last week when I read an article in the WSJ last Thursday entitled “What to Make of This Very Weird Market,” by James Mackintosh, one of the more thoughtful writers on the Journal staff. In short, he presents the case that “The market is weird. Stocks are swinging about as though there’s a full-blown crisis, while the S&P 500 is just 2% from its high.” He goes on to point out that divergence between the three best and worst performing sectors has been extremely wide (see table below), and has been present before periods of extreme market stress, such as the 2008 financial crisis, the pandemic, or the dot.com bust:

Source: OptionMetrics

And yet, despite the wide divergences, the S&P (SPY) remains within 1.5% of its highs and the VIX relatively low (<20).

To Mr. Mackintosh’s credit, he admits that the situation is “weird” and cannot recommend a preferred course, other than “ignore it, trade it, or panic” (which if you think about it, are always your three choices).

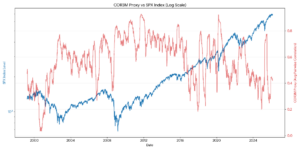

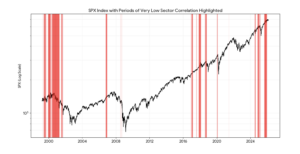

So, what’s really going on? To begin, it’s not that weird. The connection between sector divergence and the overall level of the market or as a leading indicator of extreme price action isn’t that great. Below is (a) the SPX vs. 3-month (63-day) rolling average pairwise correlation between six major sectors (XLE, XLB, XLP, XLK, XLY, and XLF), and (b): low correlation periods, highlighted, vs. the SPX:

Source: OptionMetrics

Source: OptionMetrics

As you can see, the correlation isn’t consistent and can decouple for extended periods. Like all analysis and trades involving correlation, that’s something to always keep in mind.

At the same time, sector divergence is related to the overall level of implied volatilty, in this case, the VIX. But again, the relationship isn’t consistent. In general, low correlation between sectors indicates that diversification is working, lowering overall volatilty. In contrast, during periods of extreme stress, such as during the 2008 financial crisis, sector correlation tends to drive toward 1.0 as investors sell everything. Currently, we have low correlation and moderate to low VIX levels, a “disbursement” regime in which individual sectors are acting independently of each other. In this case, some of the sectors are hedging movements in AI-related stocks.

Even if the market is acting weird (which I don’t believe it is), that’s the nature of the game. In reality, there’s always something that is behaving ahistorically, or at least not the way it “should,” that confounds conventional analysis. Although that may be frustrating for market pundits, traders, and professional investors who are paid to know what’s going on at all times, it’s actually good news for them in the long term. After all, if the market behaved according to history at all times, then anyone could trade it and make money. Be careful what you wish for!