Semiconductors vs. Software

With the war dominating financial headlines, other market developments have received comparatively little attention. Semiconductors vs software is a great example.

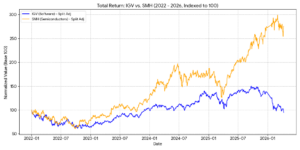

Below is a chart of IGV (the iShares Expanded Tech-Software Sector ETF) vs. SMH (the VanEck Semiconductor ETF):

Source: OptionMetrics

The sectors began to diverge in Q2 2025, driven by continued AI infrastructure buildout and expectations that AI will displace many existing software applications. The spread has been hitting record highs since mid-2025, prompting many to believe that it is due for a correction back to “normal” historical levels (i.e., mean reversion will eventually assert itself).

Maybe, maybe not. I’m usually skeptical of “this time is different,” but this may be one of those times. Recognizing a regime shift matters. Here, it’s increasingly clear that many software applications can be replicated with AI. The market may be over emphasizing that threat, but that’s a reason for a correction—not a long-term reversal. How quickly established software is abandoned for homegrown alternatives remains an open question, but seismic changes are clearly coming to the software business and the SMH/IGV spread reflects this. It’s hard to turn back disruption.

Crude Oil Rankings, Revisited

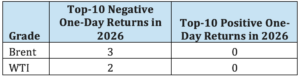

I wrote a post on March 19th for OptionMetrics entitled Crude Oil Volatilty: Not Unprecedented. In it I noted that crude oil volatility, as defined by a few different metrics, was not unprecedented and not more extreme than in certain previous periods. Most notably, the first few months of the pandemic in 2020 were considerably more volatile than the current period (and it wasn’t even close!). Is that still the case?

Mostly. Whether looking at one-day or 5-day returns, and for both WTI and Brent, March – May of 2020 still dominates the findings. But, of the top-10 most positive and negative one-day returns, 2026 now has a few entries:

Source: OptionMetrics

In addition, of the top-10 most positive 5-day returns, Brent now has one entry coming in at #8, 03/09/2026 (25.7%). Still, 2020 remains as the most volatile period ever for crude oil.

As for absolute changes in implied volatility, 2026 still does not show up in the top-10. However, one significant change from a few weeks ago is the degree of backwardation present in both WTI and Brent. Whereas before it was below the 2020 levels, it has since made new record highs (see chart below). Backwardation results from near-term supply shortages, so it’s no surprise.

Brent Crude Futures, 1-Month – 6-Month Spread