Oil: Implied Volatility is Strange

The war continues, and the supply situation for oil continues to grow more cataclysmic with each passing day. The oil forward curve and prediction markets still point to a late‑spring or early‑summer end to the war, but this week could test that assumption.

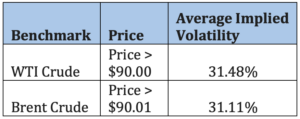

Interestingly, the current oil price spike has been accompanied by much higher levels of implied volatility relative to absolute price than during previous crises. As a general condition, oil is normally negatively correlated to its implied volatility. However, if high prices are due to a severe supply shock, then they become positively correlated. The current market is exhibiting exactly that behavior – high volatility and high prices. Currently, WTI and Brent volatility are trading 95% and 104%, respectively. As you can see from the table below, that is over 3X what it normally trades when prices are greater than $90. Although recent daily price swings are not unprecedented (March and April 2020 were greater), price vs implied volatility is. As usual in options, uncertainty is king.

Source: OptionMetrics

No Driving!

I was in San Francisco recently and noticed something on the streets that has been a long time coming: self-driving vehicles. Waymo cars, with all their spinning discs and sensors, are all over the place! Take me to your leader!

Self-driving cars are one of those technological advancements that never seem to catch on. Safety concerns, regulatory pressure, and customer hesitancy have all slowed self-driving’s general adoption. Although I’m hesitant to write this, that might finally be changing.

First, it would be helpful to define exactly what “self-driving” means. The Society of Automotive Engineers has defined four levels of self-driving from L2 to L5. L2 is only partial automation, like what Tesla has; you still have to keep your hands on the wheel. In L3, you can take your eyes off the road but still have to be involved. Waymo is L4, which almost represents full automation except that they are limited to a set area (geofencing). L5 is the stuff of science fiction. You just get in, tell the car where you want to go, and off it goes. No involvement is required after that, and the vehicle is available anytime and anywhere with no limitations. In other words, even if its pitch black and snowing, the car will still take you where you want to go. No commercial examples outside of the lab are yet available, and skeptics say they are years away. With the pace of AI development, we shall see.

Why the newfound optimism in self-driving? Mostly, it’s because the discussion has shifted from “if,” to “when,” with consequent advancements in technology and regulation. Mostly, this reflects a shift in the debate from “if” to “when,” driven by advances in technology, consumer acceptance, and regulation. Last January, the CES show was dominated by autonomous vehicles, with Nvidia introducing a software package to compete with Tesla’s. In addition, Congress introduced the Self-Drive Act that replaces conflicting state regulation with a federal framework. And finally, there is the introduction of Tesla’s Cybercab, a dedicated robotaxi, which will compete with Waymo, which tripled its number of rides in 2025 and secured $16 billion in funding last February. It’s now valued at $126 billion as a stand-alone company. That’s more than the combined value of VW and Mercedes.

Although some of the most recent developments seem like wishful thinking, self-driving is clearly inevitable. I doubt my kids, or their kids at the latest, will even know how to drive a car manually.

For now, there aren’t any pure plays in the self-driving car sector. Waymo is owned by Google, but it’s not a major factor in its revenue performance. Last year, Google’s revenue was almost $403 billion; Waymo contributed an estimated $1.0 billion, or only 0.25%. Tesla is a purer play, especially considering its Cybercab initiative and ever-advancing full self-driving (FSD) feature, but it is still essentially an auto manufacturer.

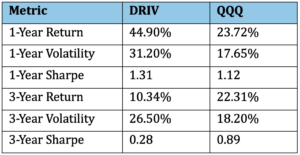

The Global X Autonomous & Electric Vehicles ETF (DRIV) focusses on “future mobility” and invests in autonomous technology, electric vehicle components, and EV materials. It’s a broad-based bet, and since most of its top holdings are mega-caps like GOOGL, MSFT, NVDA, and TSLA, it is highly correlated on a long-term basis to QQQ (about 0.83).

There’s an investment lesson here. When you view DRIV on a risk-adjusted basis, your opinion may change. Although the metrics may vary somewhat, risk-adjustment always boils down to adjusting an asset’s return by its volatility. The Sharpe ratio (asset return – risk free return/asset volatility) is the most popular. The higher the ratio, the better. Comparing the risk-adjusted returns of DRIV and QQQ, you can see that DRIV’s Sharpe ratio suffers due to its higher volatility. On a long-term basis, DRIV has not had enough return to justify its higher volatility. That leads to the conclusion that with the exception of the last 1-year period, QQQ was a more risk efficient investment, especially after fees are considered.

Source: OptionMetrics