LNG Peaking?

I’ve written about opportunities in liquified natural gas (LNG) several times, but before the new Trump administration took over. Since then, two recent developments have changed their outlook.

First, US energy policy has swung decidedly in favor of the production, sale, and processing of fossil fuels, including LNG. “Drill baby, drill!” more or less summarizes the new policy. Early last year, the Department of Energy froze all pending and new LNG export permits, pending further environmental and economic analyses. As part of his new energy policy, President Trump overturned the freeze by executive action in January. Obviously, this was bullish for energy and LNG-related stocks, such as Cheniere Energy (ticker = LNG), the largest US exporter of LNG and the world’s second-largest producer. I’ve written about Cheniere a few times, most recently here.

Second, the reordering of our relationship with Europe and Russia, which hinges on the war in Ukraine, has implications for liquified natural gas that are not obvious. By way of background, prior to the war, Europe imported about 40% of its supplies of natural gas via pipeline from Russia. This changed after Russia curtailed the supply, which led to a frantic scramble for alternative sources. Liquified natural gas, which can be transported by ship, fits the bill perfectly. After years on the energy periphery, LNG was suddenly in demand, and LNG-related stocks, including Cheniere, soared.

However, the prospect of the war somehow coming to an end (one way or another) has thrown doubt on the future of LNG and Cheniere’s prospects. President Trump has repeatedly stated that a settlement to the war in Ukraine is one of the goals of his administration. If a settlement does occur, natural gas supplies from Russia will become available again, and the necessity to import LNG over the water will become less apparent. For LNG exporters, such as Cheniere, that would not be good news.

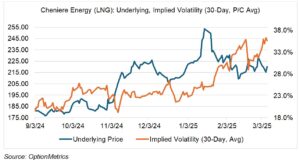

What does all this mean for LNG stocks and options? Realistically, a settlement to the war in Ukraine is most likely months, or maybe even years, away. But the possibility is hanging over the sector, moderating and limiting further upside progress. At the same time, Cheniere is suffering from broader market woes as well as post “Trump Bump” fatigue, both of which have resulted in downward pressure since its post-election peak on January 15 (see chart below). In general, and lately, LNG implied volatility moves inversely to its price, so any downside breakout will push its IV higher. For options traders, trades that can make money on both price and implied volatility are the name of the game.

I Don’t Get It!

I admit it – there are lots of things I don’t get about crypto, but there is one recent development that I really don’t get, namely that crypto will increase in value forever, and therefore should be included in any portfolio, corporate treasury, or even government reserve. This notion has been around since the birth of crypto, but the rise of MicroStrategy (now Strategy (MSTR) gave it increased traction. Reportedly, other companies are following Strategy’s business model and are now considering adding bitcoin to their treasury.

Last week, recent crypto superfan President Trump has apparently bought into the narrative with an executive order to create a “strategic crypto reserve,” composed of various crypto products. The stated intentions are varied and run the gamut from it’s a “digital Fort Knox,” to it could be used to pay down the national debt, to it could be part of a new US sovereign wealth fund, to it’s a prudent diversification vehicle.

All of these arguments assume that crypto as an asset will continue to increase in value. Since that has not been the case since bitcoin peaked in late January, the arguments in favor of including it as a reserve asset have lost their luster. As of Monday’s close, bitcoin is now down 15.8% year-to-date; both the S&P (-4.3%) and gold (-8.4%) are easily outperforming it.

As an aside, government reserves of bitcoin currently +total approximately $16.7 billion. For context, US gold reserves are currently valued at $757 billion (using $2900/oz). Although that’s a big number, keep in mind that the US has been off the gold standard since 1971 and has not intervened directly in the markets to maintain the value of the dollar since the early 80’s. The function of the gold reserve is at this point purely symbolic, reassurance that there is something hard and real standing behind our currency. I doubt a crypto reserve will provide additional confidence.

And Finally, Tesla

As of Monday’s close, Tesla (TSLA) is down 41.4% year-to-date. Disapproval of Elon Musk’s high political profile (when does he have time to run all his companies?) are apparently contributing to this year’s Tesla bonfire. Given his current worth of about $330 billion (he was worth north of $430 billion just a few weeks ago – what’s $100 billion between friends?), I’m pretty sure losing money personally doesn’t concern him that much. It brings to mind the famous line from Citizen Kane, when Charles Foster Kane is berated by his banker and former guardian for investing in newspapers:

“I expect to lose a million dollars this year. I expect to lose a million dollars next year. You know, Mr. Thatcher, at the rate of a million dollars a year, I’ll have to close this place in… sixty years”.

More on TSLA next week, as well as the failsafe arbiter of questionable economic policies, the market.