It’s Not That Volatile!

As I’ve been writing for the last year or so, never-ending economic and geopolitical uncertainty is dominating the markets. This was true even before war broke out with Iran, and is now indisputably the single most important factor affecting all asset classes.

Understandably, this had led many to conclude that the markets are now more volatile than they used to be. Abnormal price swings due to unexpected news, whether it be economic, financial, or political, are said to be so common now that they are the “new normal.”

Although this seems intuitively true, is it really correct?

To find out, we reviewed two equity indexes, the SPX and the VIX, and a commodity that is front and center in the news, crude oil (WTI). Subjectively, we defined “historical data” as the period from 01/02/1996 – 12/31/2024 and “recent data” as the period from 01/02/2025 – 02/13/2026. For crude oil (WTI), the series began in 2005. We then calculated various metrics that are usually indicative of higher volatility.

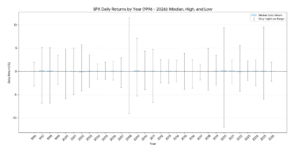

First, the SPX. If the markets were truly more volatile during the recent 2025/2026 period, then one would expect a wider range in daily returns (see chart below):

Source: OptionMetrics

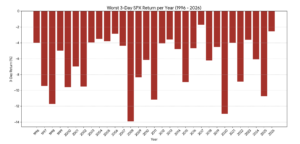

In addition, since many unconsciously equate volatility with downside risk, one would also expect worse downturns (see chart below):

Source: OptionMetrics

As you can see, both charts do not indicate extraordinary volatility during the 2025/2026 period when compared to the rest of the historical series. This is especially true in comparison to the dot.com, financial crisis, or pandemic periods.

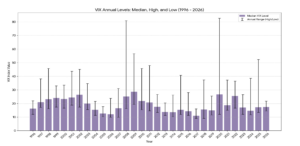

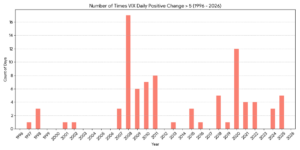

Second, we examined similar metrics for the VIX:

Source: OptionMetrics

Source: OptionMetrics

The VIX displays more evidence of increased volatilty in the most recent period, especially 2025,

than did the SPX using similar metrics. In particular, the highest VIX reading of 2025, 52.33, was only exceeded during the height of the financial crisis and the pandemic. The number of spikes greater than 5 in 2025 also indicates heightened volatilty. However, although that is true, the performance of the VIX during 2025 and 2026 is not extraordinary.

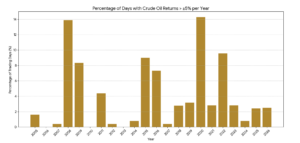

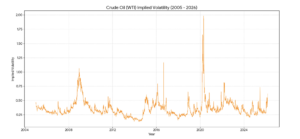

Finally, we reviewed crude oil (WTI) since it has once again been thrust into the limelight by the war in Iran (see charts below).

Source: OptionMetrics

Source: OptionMetrics

As was the case with the SPX and VIX, crude oil has not displayed extraordinary volatility during 2025 and 2026 (at least so far).

Given all the data we examined, is the market really more volatile recently? It’s important to differentiate perceptions of increased volatility with actual conditions. Given the two time periods reviewed, volatilty in the most recent period is indeed higher, but only marginally so and not to the extent that it can be considered to be historically unique.

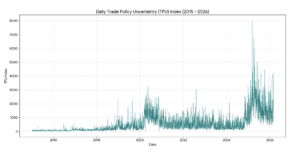

In this case, many could be confusing uncertainty with volatilty. As you can see below, economic policy uncertainty has been at record highs since late-2024. However, that doesn’t necessarily mean that volatility is higher, just that overall conditions are more uncertain. The two should not be confused.

Source: https://www.policyuncertainty.com/index.html