Is the Market More Volatile?

Recency is the cognitive bias to overweight recent events when making a decision. Although investors acknowledge that it’s important to review conditions more than just a few years back, they often just can’t escape the 24-hour news cycle. The result is that they tend to view current events as more extreme, unique, and volatile than what has occurred in the past. Since the current administration came to power in 2024, there has been a never-ending stream of screaming headlines, some of which affect the markets and all of which contribute to a general sense of unease and uncertainty. This leads to the conclusion that the markets are more volatile and risky than in the past and that the VIX is “too low.”

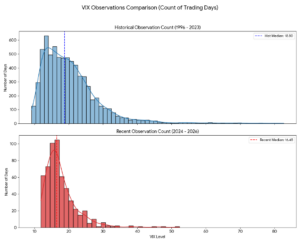

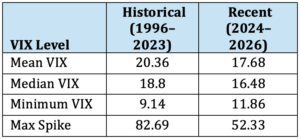

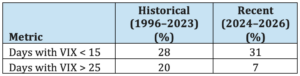

Is this true? To find out, we compiled several views comparing the VIX in 1996 – 2023 to 2024 – 2026:

Source: OptionMetrics

Summarizing,

Source: OptionMetrics

Source: OptionMetrics

What do we make of all this?

- The mean and median for the 2024 – 2026 are lower when compared to the earlier period. That’s not surprising since the VIX spiked during thedot.com, financial crisis, and pandemic eras.

- However, the frequency distribution of the current period has shifted right, indicating that the VIX is reflecting higher baseline uncertainty.

- In general, the current distribution is “spikier,” i.e., the observations are clustered around the median. Surprisingly, the number of days > 25, which could be considered a spike, is less than the historical frequency. 2024 – 2026 has had frequent shocks but nothing on the magnitude of those achieved in the historical sample.

Evidently, recent market volatility, as measured by the VIX, is not more volatile than previous periods. However, one interesting side note. As you can see below, VIX spikes > 25 have become increasingly short-lived. Spikes occur, but calm down after about a week. A combination of the “TACO” trade and the increasing popularity of “buy the dip, let her rip” might account for this.

Source: OptionMetrics