Is KOSPI a Bad Omen?

If you’re interested in potential bubbles, you need look no further than the South Korean equity index, the KOSPI. Record highs, extreme volatility, hyper-concentration, leverage, retail excitement, and an institutional vs. retail rift – the KOSPI has it all.

What’s going on and is it important to US investors?

For the uninitiated, the KOSPI is the Korea C\omposite Stock Index, which tracks all common stocks trading on the Korean Stock Exchange. Since it is a market-capitalization-weighted index, the KOSPI is heavily concentrated in AI-related and memory chip issues. Samsung Electronics and SK Hynix currently make up about 52% of the KOSPI 200, but their share has recently been as high as 60%.

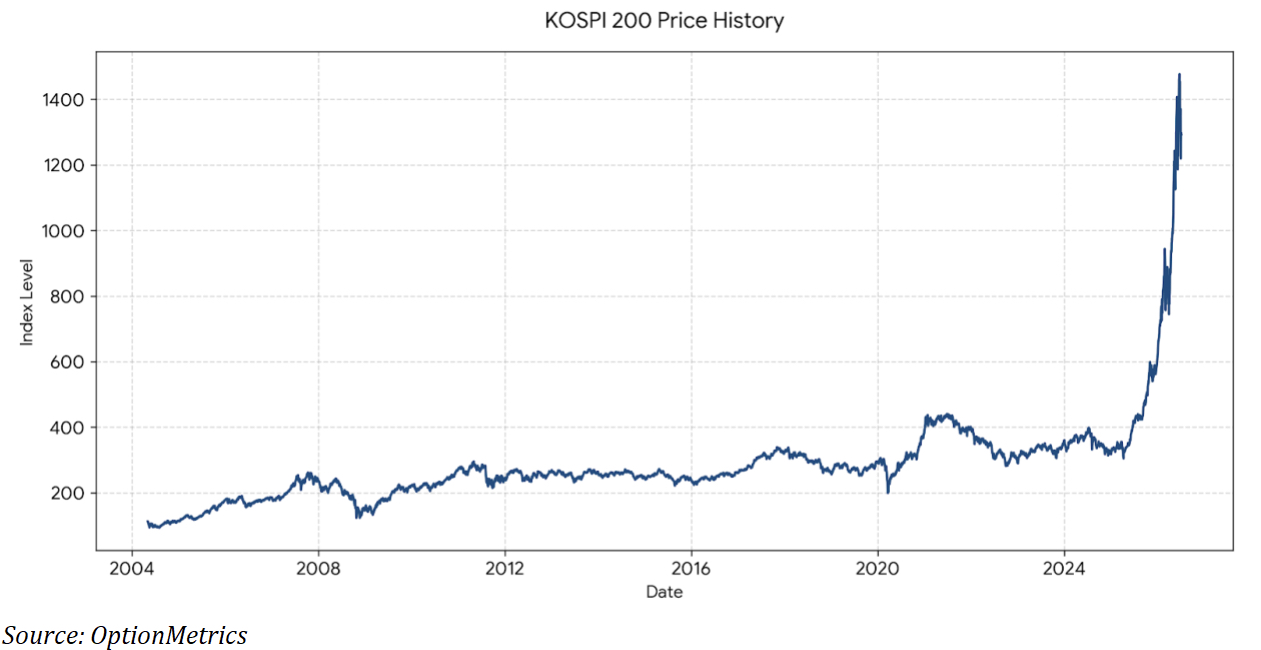

Consequently, the KOSPI is now over three times what it was at the end of Q2 2025 and as of last Friday was up over 113% year-to-date:

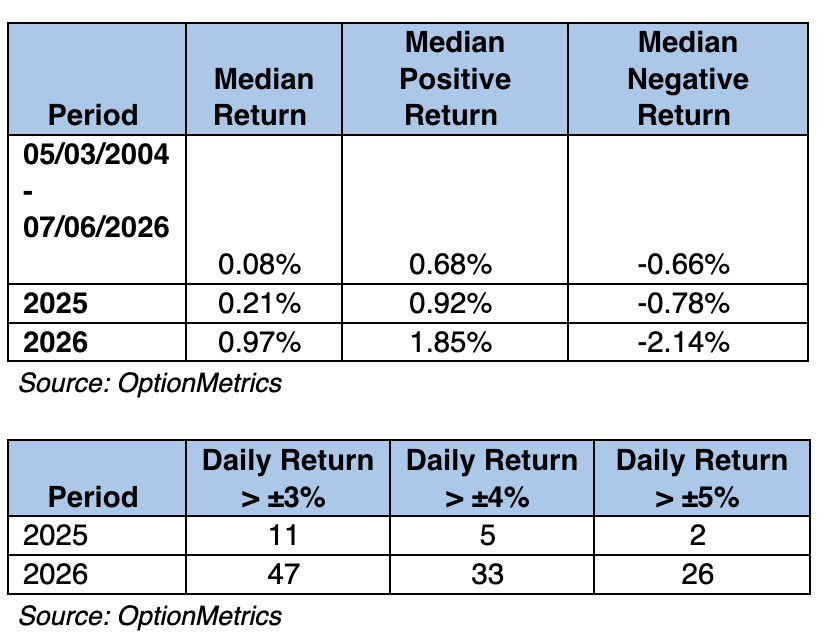

Naturally, this was accompanied by higher daily returns and swings:

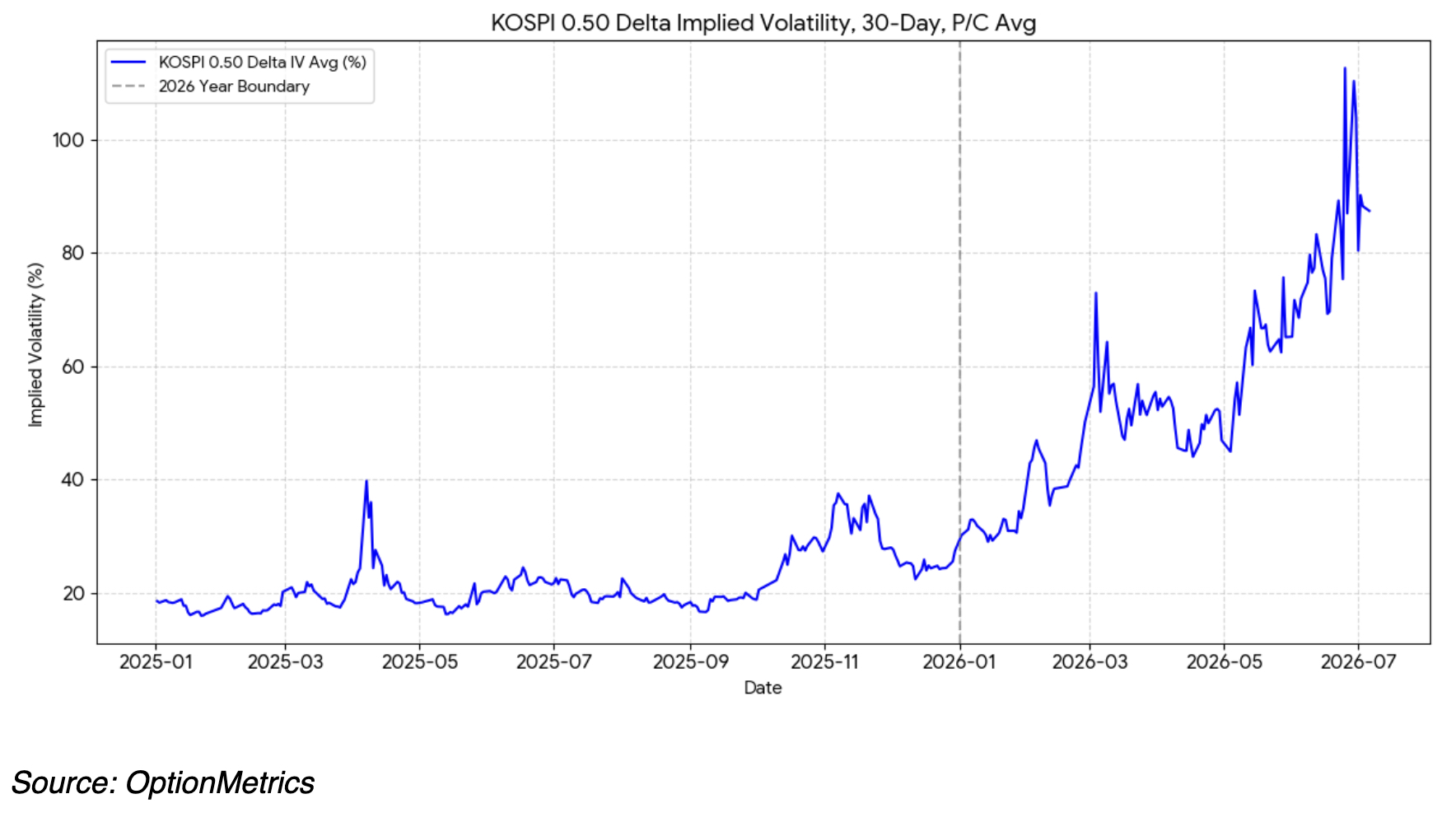

This has led to an explosion in KOSPI’s implied volatility:  As you might expect, retail (popularly known as the “Korean Ants”) is on the march and isn’t scared of levered products or margins. Korean regulators report that 92% of the buyers of single stock leveraged ETFs in Samsung and SK Hynix are retail investors. At the same time, retail trading accounts opened by minors have expanded nearly tenfold compared to just last year (question: why can a minor open a brokerage account, ever?).

As you might expect, retail (popularly known as the “Korean Ants”) is on the march and isn’t scared of levered products or margins. Korean regulators report that 92% of the buyers of single stock leveraged ETFs in Samsung and SK Hynix are retail investors. At the same time, retail trading accounts opened by minors have expanded nearly tenfold compared to just last year (question: why can a minor open a brokerage account, ever?).

South Korean margin debt has ballooned to record levels. As of mid-June, outstanding margin loans were up almost 40% from end-2025; unsecured loans also surged. Credit to trade Samsung and SK Hynix accounted for almost a quarter of the increase. Over the past six months, margin borrowing linked to SK Hynix was almost five times higher, while borrowing tied to Samsung was almost three times higher.

Highly levered markets with mass retail participation are highly susceptible to sudden downward price shocks. Disappointing or unexpected fundamentals, or an increase in margin requirements, can force a cascade of deleveraging as traders are forced out of their positions. This has been evident since mid-June. As of last Friday, the KOSPI was off 11.4% from its mid-June highs.

Fearing an overcooked market, foreign institutional investors have been heading for the exits and have unloaded about $103 billion in equity since the beginning of the year, a record for South Korea. At the same time, the retail Ants have stepped up to absorb the outflow, setting up a clear retail vs. institutional divide.

Explosive price increases, frantic retail participation, levered ETFs, institutional flight, and high margin debt. What could go wrong?

Could these factors cause a panicky to sell off in KOSPI that spreads to US markets? So far, the risk of contagion is probably small. Korean financial regulators and the Bank of Korea seem determined to put the fire out by forcing domestic brokerage houses to freeze new margin lines, hike maintenance requirements to 100% on certain stocks, tighten suitability standards, and allow automated margin calls. In other words, all the stuff they should have been doing all along. Regardless, we’ll find out soon whether they’re too late to stop the march of the Ants.

The Semiquincentennial

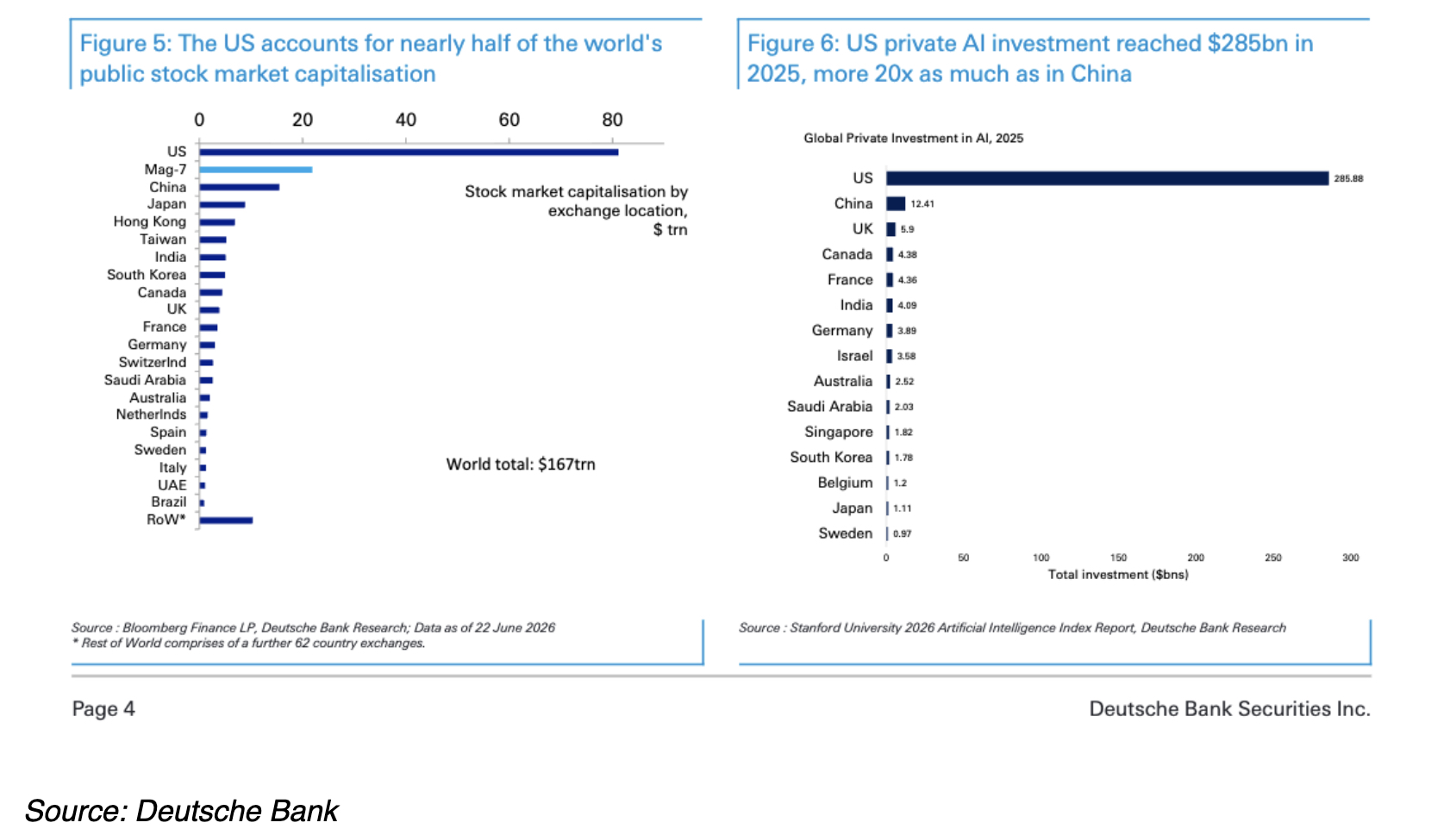

On June 24th, Deutsche Bank published a report entitled “US at 250 – Why has the US been so successful and can it continue?” Short answer: “…the case for the US as the world’s pre-eminent investment destination remains intact. An investor into the US buys a bundle that is hard to replicate – productivity leadership, the deepest and most liquid capital markets in the world, the rule of law that underpins them, and the flexibility conferred by the dollar’s reserve role. That combination should persist.”

Below are two of the more interesting displays in the report. As you can see, US financial markets continue to dominate broadly and specifically:

Evidently, Wall Street and the US are still on top, and it’s not even close.