Implied Volatility Isn’t All That Accurate!

Anyone who reads the OptionStrat blogs regularly knows that implied volatility is the Holy Grail of options pricing. Talk to any institutional options trader, and it’s all they talk about. Which leads to an obvious question: just how accurate is implied volatility in forecasting price variation? And if it’s not that accurate, why do we keep on using it?

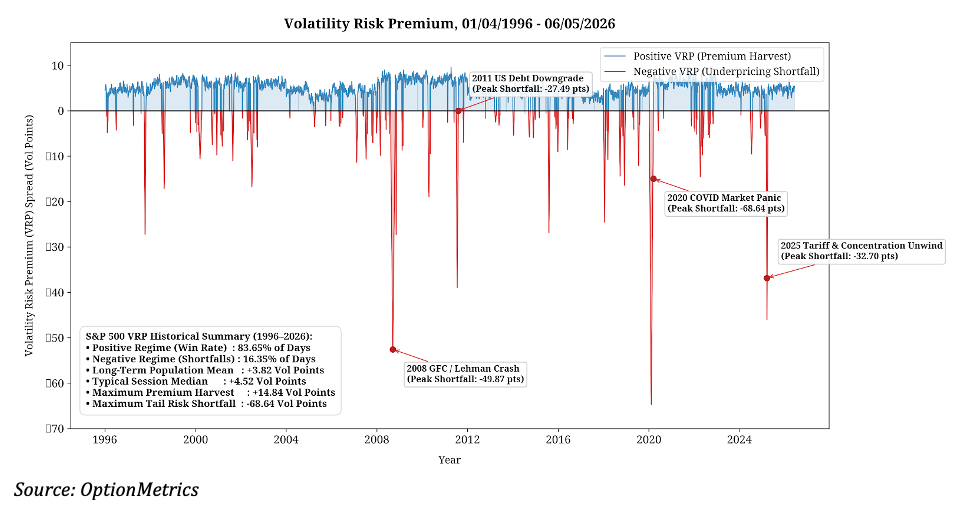

To find out, I reviewed VIX and SPX data going back to 01/02/1996. I then compared implied volatility on a specific date against future realized volatility (i.e., the annualized standard deviation of daily SPX lognormal returns) over the next 30 days (approximately 21 trading days). The result is the forward-looking volatility risk premium (VRP). Note that this is the opposite of the exercise in which past realized results are compared to the current implied volatility, mixing backward-looking metrics (historical realized volatility) with forward projections (implied volatility).

The chart below displays the results:

As you can see, implied volatility exceeds the market’s realized results almost 84% of the time and by an average of 3.82 percentage points (the blue line above). That’s almost 20% of the average VIX and 25% of its median. In other words, implied volatility consistently overstates realized forward results and consequently the VIX contains a significant cushion for volatility sellers.

So, implied volatility doesn’t seem to be that accurate when compared to actual results. But that’s not really the point.

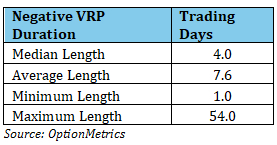

Why? Think of options like insurance. Institutions (pension funds, endowments, short volatility ETFs, and certain hedge funds), as well as some retail investors, use options as an insurance-like product to protect against extreme left-tail events while producing steady returns. Like all insurance, the prices are padded to take into account asymmetric downside risk (so-called “Black Swan” events). Almost always, sellers get to keep the built-in cushion (and that’s a good thing – I have never once filed a claim against my overpriced fire insurance, but at the same time I don’t want my house to burn down). Sellers have another advantage as well – instances in which realized results exceed implied volatility and a negative volatility risk premium results are usually short-lived. Using the table below, the median length is just 4 trading days.

Of course, systemic regime shifts, such as those caused by the 2008 financial crisis or the pandemic, can cause much longer negative VRP periods, but such radical shifts are relatively rare.

It shouldn’t be much of a surprise that implied volatility is an imperfect predictor of actual variance. After all, the level of implied volatility is a guess based on historical price variation and experience; no one can tell the future. And be careful what you wish for — if it were a perfect estimate, then there wouldn’t be much options trading in the first place because sellers wouldn’t show up. Yes, implied is overpriced most of the time, but it makes the options market work.

SpaceX, Again

As I wrote last week, SpaceX options are set to begin trading today (Tuesday, 06/16/2026). Given it’s stratospheric performance since its debut last Friday, there is already talk of a “gamma squeeze” (investors buy calls and sellers hedge them by buying the underlying). Expect triple-digit volatility and high, frantic volume until the early adopters settle down. I will review the early action in next week’s blog.

One interesting point I didn’t make when I wrote about SpaceX last week. Perpetual markets (“perps”), i.e. the 24 X 7 variety common in crypto and available offshore, have branched out into certain equity and commodities, SpaceX among them. SPCX original IPO price was set at $135, but to anyone viewing the perpetual markets, the stock had been trading north of $150 and as high as $185 since the beginning of June. On the day of the IPO, but before it began trading on the Nasdaq, it was trading between $170 and $185. 24 X 7 markets are coming, like it or not.