Highflyers!

Intel (INTC) and Micron (MU) fly high. Intel, left for dead as a sclerotic dinosaur with a long history of disappointing performance, is now suddenly the latest IT prom queen; Micron, the maker of chips beset by oversupply and commoditization, has shot over 3X in just the last two months. As you would suspect, the mega trend of this decade, AI and its insatiable appetite for chips, is propelling them both. Other chip makers, such as Samsung, SK Hynix, SanDisk, and

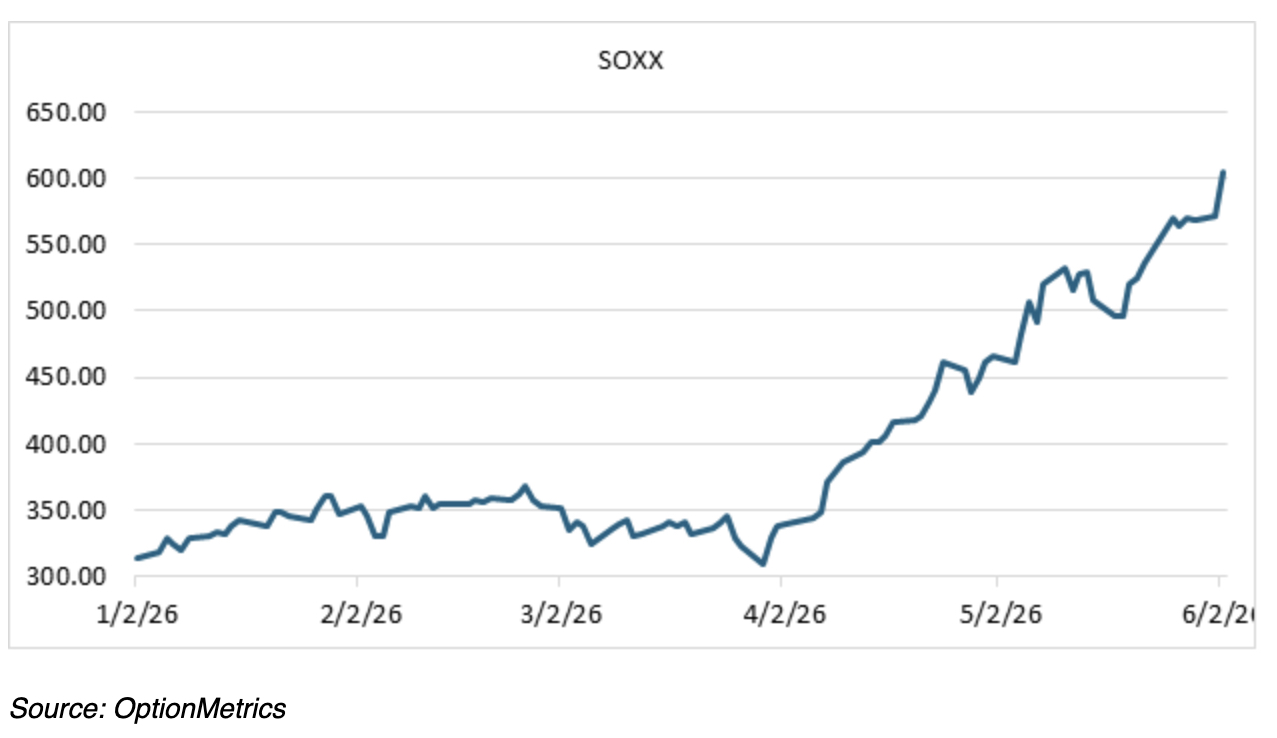

Advanced Micro Devices, to name just a few, have joined the hottest rally so far this year. As of June 2nd, the iShares Semiconductor ETF (SOXX) was up almost 92.9% ytd, 81.7 percentage points higher than the S&P (SPY).

AI-related rallies are nothing new. However, what’s interesting here is that the chip rally really took off at the end of March as the market rotated out of software-related stocks; next-gen chips were announced, and seemingly endless AI-related demand. The SOXX ETF has exploded since in Q3:

Naturally, this has led some to wonder whether the chip market is overheating and forming a bubble. They are in the “too far, too fast” camp (and have been for the last few years) and point out the off-cited resemblance to the dot.com tech bubble. They also warn of increasing competition, ever-changing technology, and high capex loads that could hobble individual chip manufacturers. At the same time, supporters point out that chip-related revenues are real and increasing, and that AI’s potential will lead to every-increasing demand.

Interestingly, both sides can be right – the market could be overbought in the short-term and eventually correct while the long-term fundamentals could also be valid and real.

I am not going to add anything original to the fundamental arguments for or against Intel, Micron, or chips in general. You could spend several days of your life researching various articles, blogs, and videos on the subject. Most of those focus on technology and underlying prices, not options valuation. Let’s concentrate on the latter.

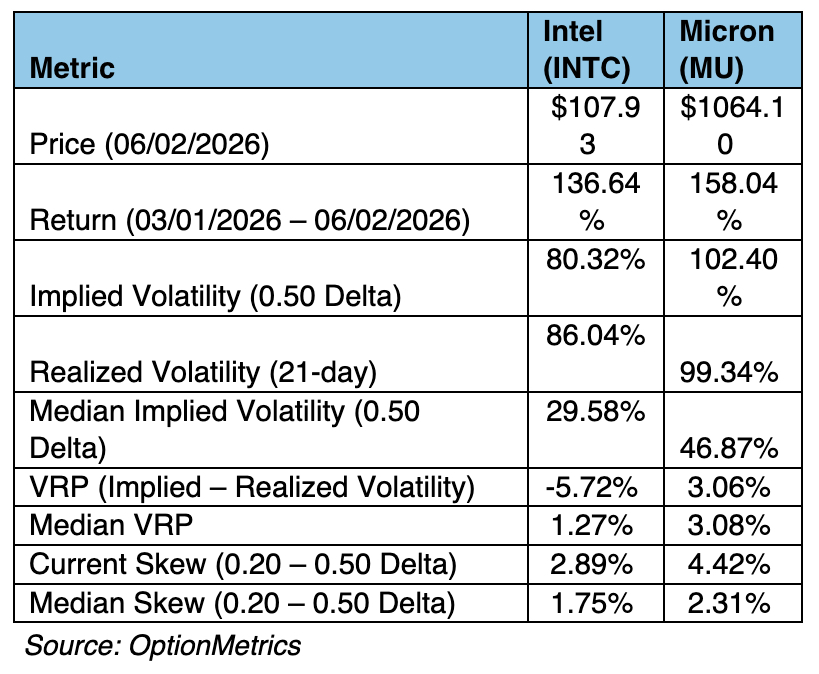

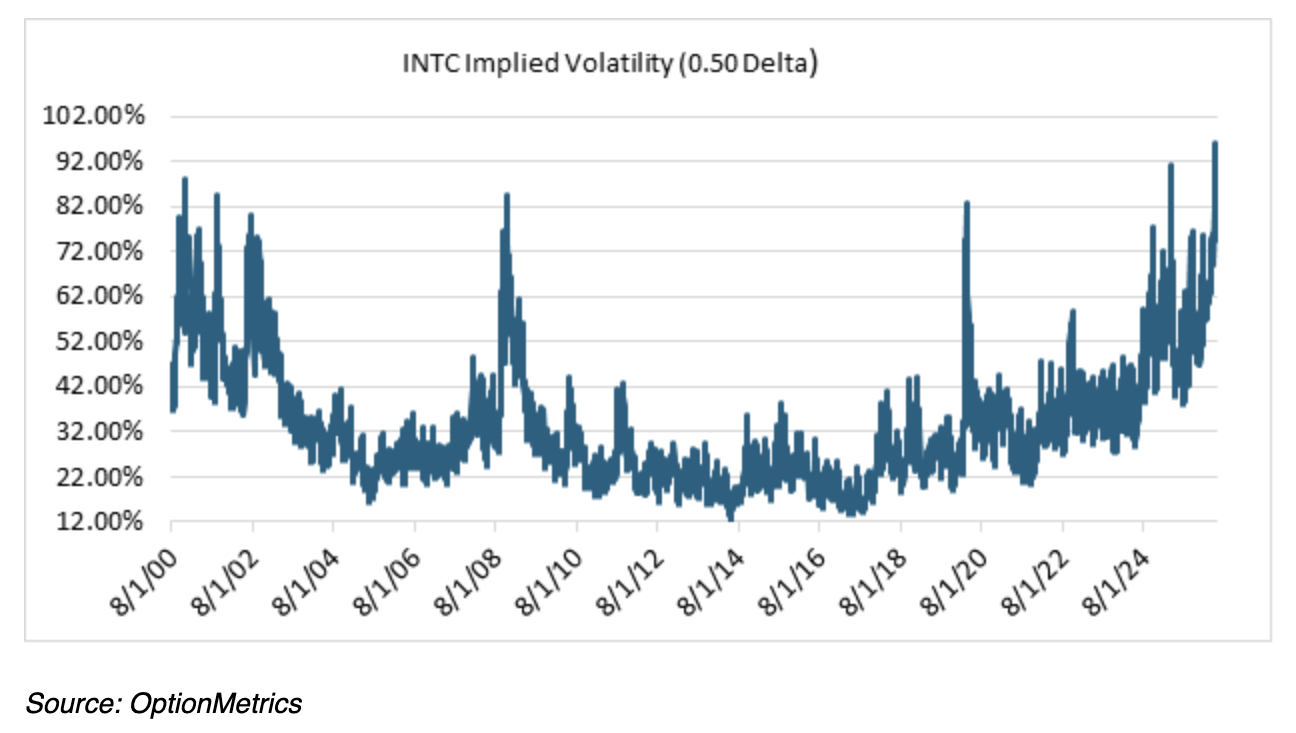

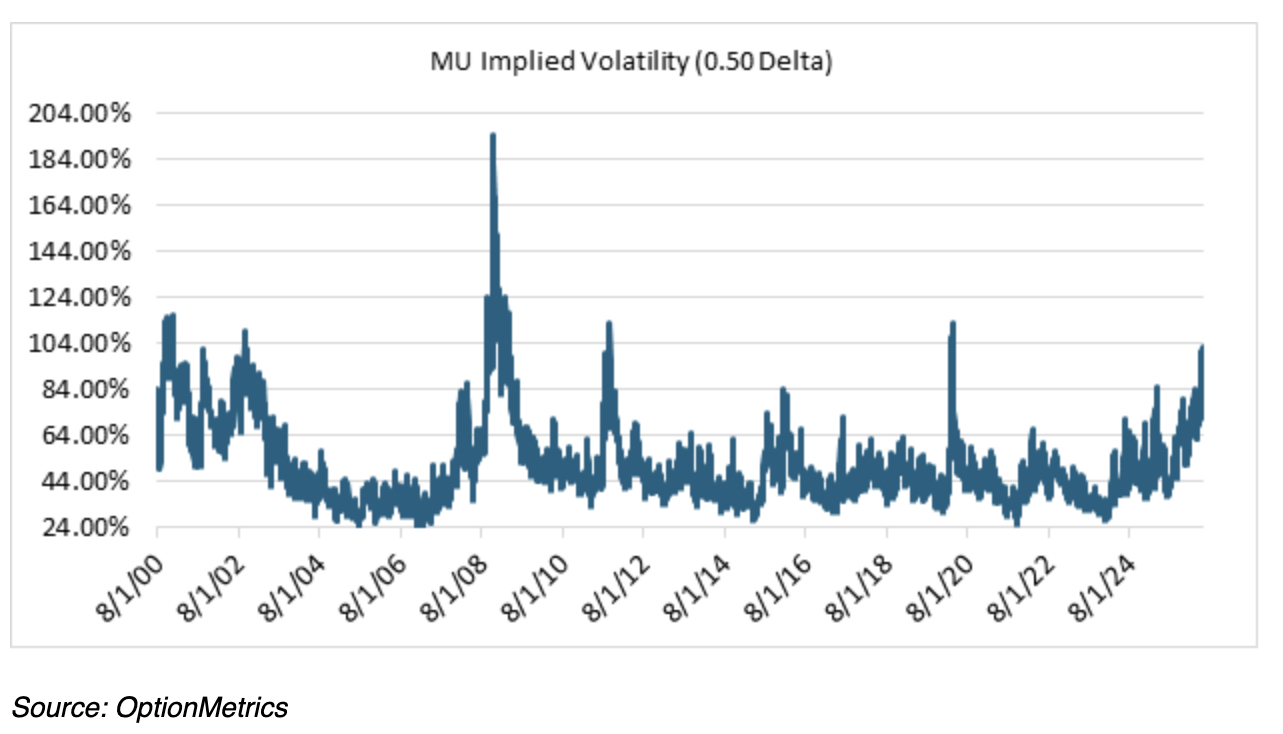

Below are some assorted options statistics for both stocks as well as charts of their respective implied volatilities:

As you can see, by any measure, SOXX, MU, and INTC options are expensive. INTC implied volatility is at record highs, even higher than the levels reached during the pandemic and the financial crisis. MU 0.20 – 0.50 skew is almost twice that of its median level. Of course, given their realized volatilities, significantly higher implied volatilities are justified, but the question is whether historically elevated levels and skews are a sign that the market is overheated. If the chip rally fades, or even loses momentum, the elevated implied volatilities will return to more normal levels. In that scenario, INTC and MU option bulls may have both price and implied volatility working against them. Buying overpriced options in the hope that they will get even more overpriced is, as my risk management colleagues put it, “sub-optimal.”

One interesting trivia tidbit about Micron – it has a connection to McDonald’s. J.R. Simplot, who dropped out of school in 8th grade and went on to become a billionaire by supplying McDonald’s with frozen potatoes, was one of Micron’s original angel investors. He recognized that Micron’s main product at the time, memory chips, was bound to become a high-volume commodity, just like his potatoes. His $1 million investment in 1980 was worth over $4 billion when he cashed out in the mid- ‘90s. Question: how many investors in 1980 would have considered investing in a Boise-based startup, much less even knew what a memory chip was in the first place? Amazing.