Crude Oil Volatility: Undervalued?

Last week, I reviewed the relationship between historical (realized) and implied volatility using the VIX as an example. Given the war in Iran and crude oil’s importance as drivers of the current market, I thought it would be instructive to conduct a similar analysis for crude oil (Brent and WTI).

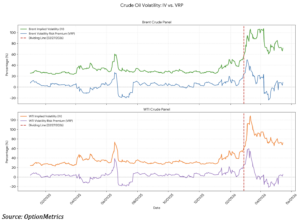

Below is the implied volatility and risk premium (i.e., 30-day P/C implied – 21-trading day historical (realized) volatility) for Brent and WTI from 01/02/2025 – 05/15/2026. The dashed line is when the war started.

As expected, the war significantly increased crude oil’s implied volatility, and at least for a little while, its risk premium. Notice that after crude peaked and did not live up to the most bullish forecasts, its risk premium quickly declined back to pre-war levels and closely mimicked the direction of implied volatility.

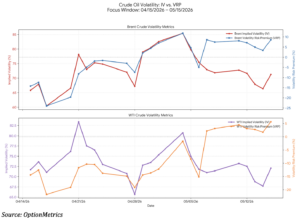

However, since early-May, crude oil’s implied volatilty and VRP have diverged (see chart below) and the VRP started increasing again:

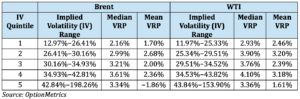

Since early May, the VRP for both Brent and WTI have increased significantly. To illustrate how elevated these levels are, the table below shows quintiles for implied volatility and the VRP since 2008 (Brent) and 2005 (WTI):

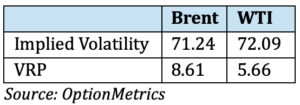

Current levels, 05/15/2026:

As the two tables above show, both VRPs are significantly above their long-term average and median levels. In fact, Brent’s current VRP is nearly 2.6x its long-term median. Why does that matter? In this case, the elevated VRP suggests that the crude market is pricing in substantial tail risk tied to either an escalation of the war or an end to the ceasefire. Although implied volatility remains well below the top of its historical range, that should not be taken to mean the oil market is complacent about the conflict — the VRP is signaling something different. Given how precarious the situation remains, that’s understandable.

One interesting note about the VRP quintile table above. Notice that the VRPs taper off or even turn negative in the highest implied volatility quintile. This indicates that WTI and Brent are subject to explosive short-term price moves in which implied volatility at first expands but soon decreases, allowing realized volatility to catch up, thereby reducing the VRP. As an example, this occurred in the early days of the war when VRP spiked but then soon came off.