Crude Oil Didn’t Cooperate

If I sent you back in time and asked you what the price of oil would be if a major war broke out in the Mideast, the Strait of Hormuz was closed, and the world was facing an unprecedented supply shortage, you probably would have guessed that crude was going to be above $150, or maybe even higher. Just a few weeks ago, you would have been hard pressed to find anyone who disagreed with that opinion.

As I’ve often cautioned, 100% consensus opinions should be viewed skeptically, and crude oil turned out to be no exception. All the dire predictions of prolonged shortages, triple-digit oil, and economic calamity were just plain wrong (there’s no other way to put it). Consequently, by several different measures, crude oil did not live up to expectations — 2008 and 2020 still hold almost all of the all-time records.

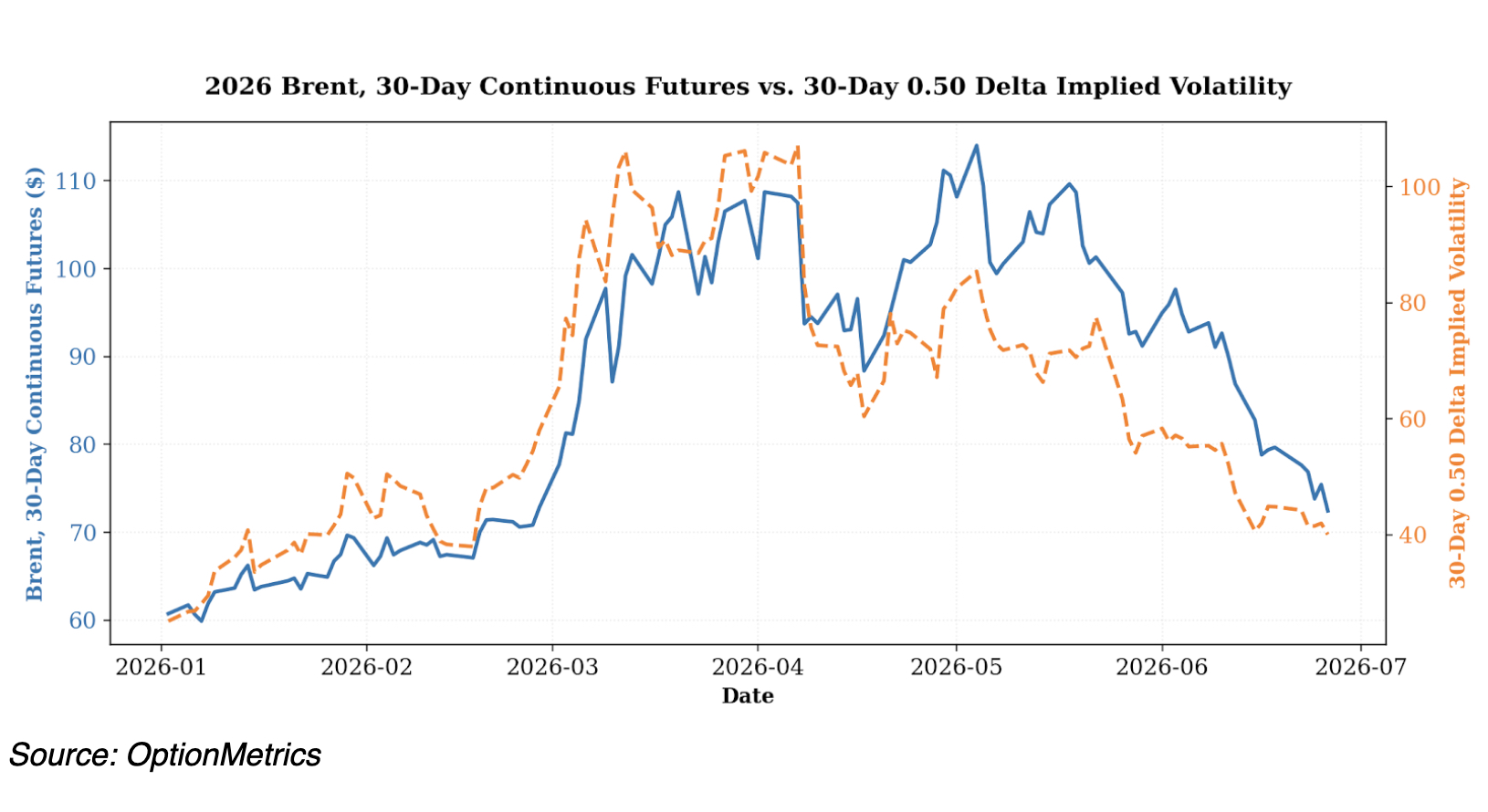

1) Brent (30-day continuous) closed last Friday at $72.45, 36.4% lower than its peak of $114.01 reached on May 4th. Historically, the peak did not even make it into Brent’s Top-10 highest readings. As a matter of fact, since 03/04/2008 it was only the 288th highest.

2) Since the war began, the largest daily swing of -12.8% was recorded on April 8th. Although this seems large, it was only the 10th most extreme.

3) Brent’s implied volatility peaked on April 7th at 107.6%, which puts it at only the 17th highest level. The following day, April 8th, it plummeted 24.2 percentage points to 82.91%, the 5th largest daily swing.

As the chart below shows, when Brent peaked in early May, implied volatility was 20 to 25 percentage points below its initial shock levels. By then, persistent cease-fire headlines had been absorbed by the market, and it was becoming clear that the extreme upside scenario was not materializing.

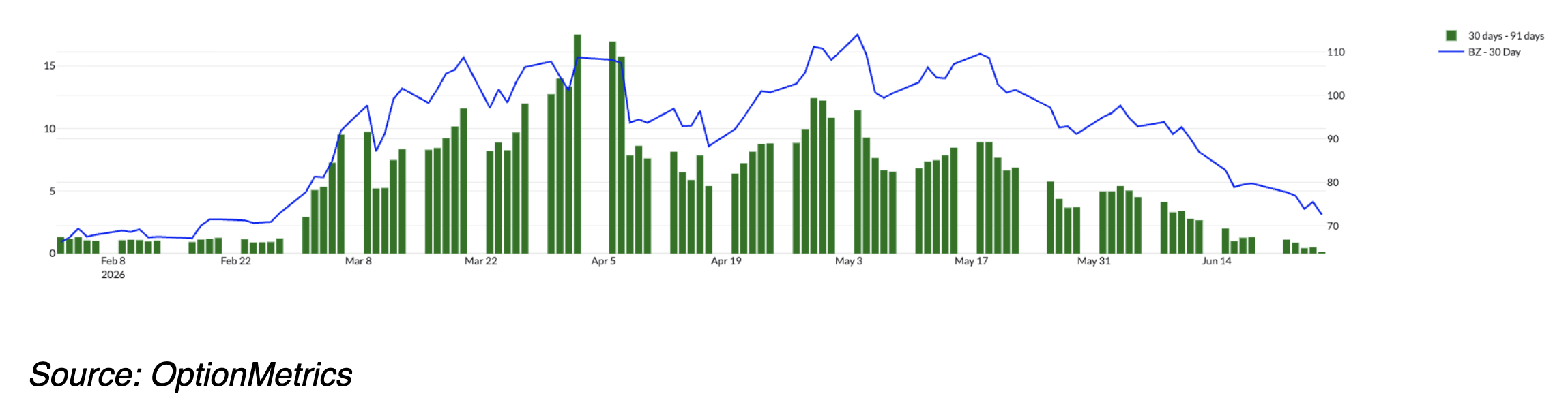

In addition, the spread between nearby and more deferred futures contracts, which were indicating extreme supply shortages, peaked in early-April and has been declining since (see below). The “normal” curve shape for crude oil is backwardation; i.e., front contracts are more expensive than deferred. The more backwardated, the tighter the supply situation and the more bullish the market (generally).

In addition, the spread between nearby and more deferred futures contracts, which were indicating extreme supply shortages, peaked in early-April and has been declining since (see below). The “normal” curve shape for crude oil is backwardation; i.e., front contracts are more expensive than deferred. The more backwardated, the tighter the supply situation and the more bullish the market (generally).

Of course, things could still be reversed as negotiations stall or are terminated altogether. Crude oil tail risk remains high, as reflected in Brent’s elevated at-the-money to out-of-the-money skew. Currently, the 0.50/0.20 delta skew stands at 3.25% and has been hovering near there since mid-June. That’s considerably higher than its long-term median of 1.39%. Apparently, tail risk is still a factor for crude and indicates that the options market is still pricing in possible upside shocks.

Of course, things could still be reversed as negotiations stall or are terminated altogether. Crude oil tail risk remains high, as reflected in Brent’s elevated at-the-money to out-of-the-money skew. Currently, the 0.50/0.20 delta skew stands at 3.25% and has been hovering near there since mid-June. That’s considerably higher than its long-term median of 1.39%. Apparently, tail risk is still a factor for crude and indicates that the options market is still pricing in possible upside shocks.

One final note. Although crude oil did not act according to the pessimist’s most dire predictions, gasoline did not disappoint. As of the end of the first half of 2026, gasoline (RBOB continuous futures contract) was the top-performing mainstream commodity, up 68.5% year to date. Technically, Sulphur beats it out at 138.6%, but industrial commodities are generally unavailable to investors or traders not directly involved in the business.